Cursed Money

Undeserved Wealth, Unobtainable Real Estate, and Unbridled Government Debt Backed by Bitcoin

Wealth can be a curse for those who didn’t earn it. Over 90% of wealthy families are likely to squander their money by the third generation. Sumptuous livelihoods are a trap without the necessary income to sustain them.

In the early 20th century, the Osage Indian Nation was blessed with substantial oil deposits underneath the land bequeathed to them by the Federal government. Never mind that the Osage were forcibly displaced from their homes in Kansas to a desolate territory in northern Oklahoma. Regardless of the means of ownership, the Osage were entitled to the land’s mineral rights and accumulated considerable wealth through drilling royalties. For a time, the Osage were the richest race of people per capita on Earth.

This stroke of luck turned into a brutal malediction as the “sudden wealth syndrome” plagued the nation with paranoia, isolation, and very irresponsible spending habits. Jealousy of the wealthy Osage by outsiders incited the Reign of Terror, where the tribe suffered manipulation, fraud, and a string of murders that prompted one the first FBI investigations. Their wealth proved to be a detriment, as it was squandered, stolen, and created animosity that provoked extensive death and suffering.

Undeserved wealth can lead to tragedy. It is the impetus for the sins of greed, gluttony, and sloth while triggering the envy and wrath of those around us. For this reason, money obtained without personal exertion, or wealth managed imprudently, can be an equivocal curse.

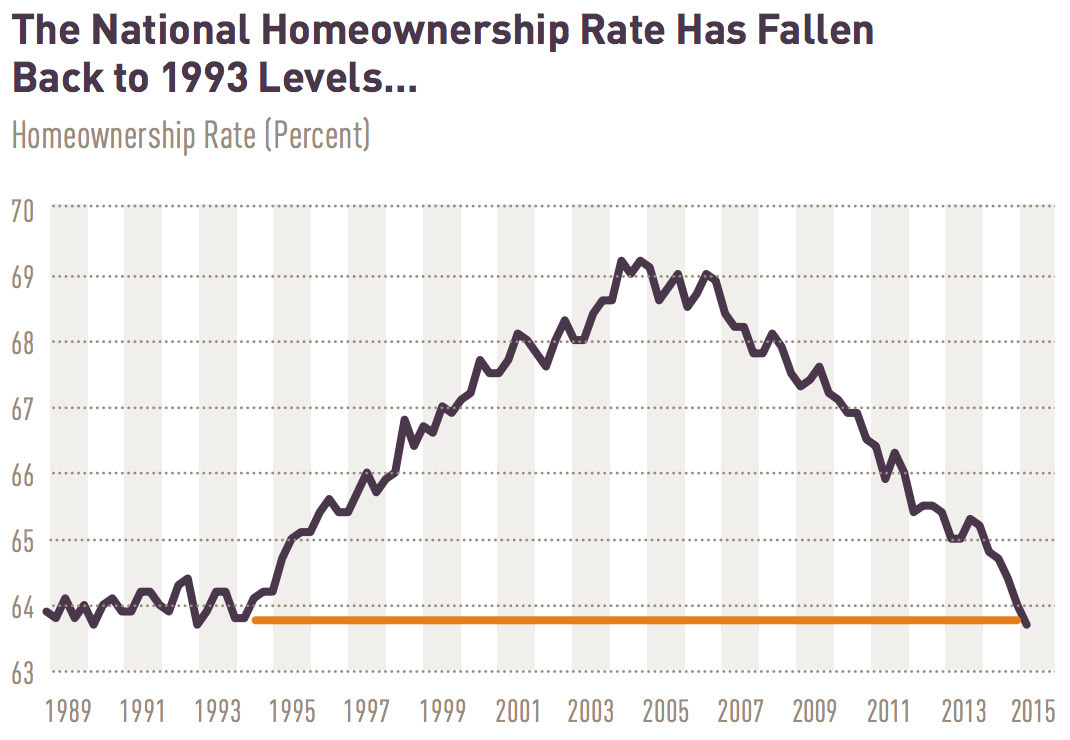

More broadly, an entire generation of Americans watched their wealth rise exponentially for simply existing. Our government’s commitment to mounting obligations and ballooning debt created an inflationary environment that enriched the holders of financial assets and real estate. The modern monetary theory that augmented the financial supremacy of our nation is a generational curse as homeownership and wealth-building become a fleeting dream for our children.

We like to come up with palpable reasons for the impossible reach of viable real estate. There are considerable factors that go into the cost of building and subsequent price of each home:

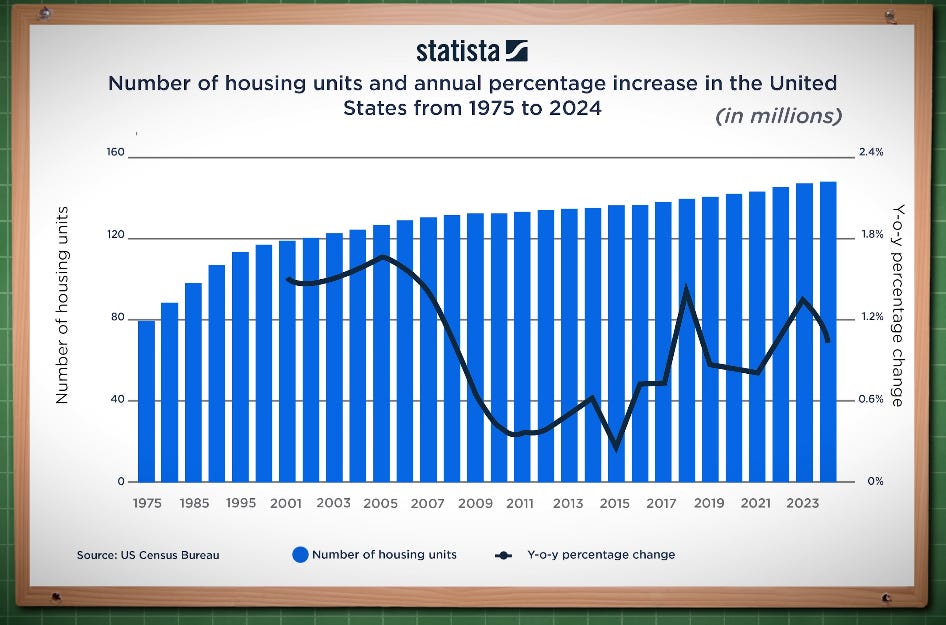

Inventory – The supply of homes heavily contributes to the market, but building has kept up with our rising population even with the increasing number of immigrants (legal & illegal). This issue is not the amount of available homes but the amount of affordable homes. The only profitable builds are intercity luxury apartments with no space or suburban McMansions with substantial commutes.

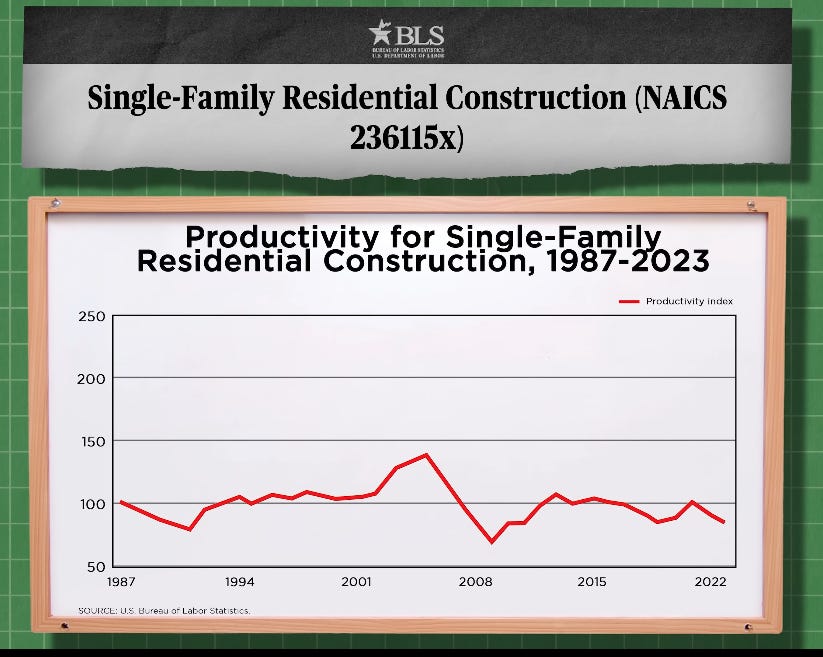

Building Costs – Manufacturing affordable houses is difficult with the inflated cost of building materials and regulatory burdens. Ironically, low construction costs are also highly dependent on cheap immigrant labor. Lesser-known reasons come from private equity ownership that has saddled homebuilders with significant debt burdens. This has collectively led to a multidecade stagnation in homebuilding productivity.

Interest Rates – The housing market is very sensitive to interest rates, as most homes are bought with borrowed money. Mortgage rates follow 10-year Treasury bond yields, which are considered the “risk-free rate.” This can be manipulated by the Federal Reserve by moving the Fed Funds Rate, which is supposed to be the cheapest and easiest way for banks to get interest on YOUR deposits. Banks must be incentivized to make mortgages even though they create the money out of thin air and carry zero risk from government subsidies…

While the above factors contribute to short-term swings in the price of homes, none are allusive to the primary long-term rise in real estate prices: pride and belief in the value of one’s home.

The existing homeowner, the seller, creates the price, and they are subject to the curse of undeserved wealth. Home equity is a self-fulfilling figure that represents faith in the value of any given property. As the currency inflates, communities are gentrified, and the desire for well-built homes in good locations rises, your home becomes more valuable despite its physical depreciation. We now consider homes to be an investment that we expect to make money from.

The existing homeowner is always at the advantage because they accumulate equity, which is far in excess of their actual principal paid down on the loan, and roll it over into a new home. In comparison to the potential new homeowner, they are making more money on each sale and essentially paying less for each new home.

The system feeds itself, as every new homeowner instantly becomes faithful to the scheme that their home is worth more every year. Their lenders and property tax assessors will incessantly remind the homeowner how much their home is worth so they will be perpetually incentivized to utilize their equity.

The equity is undeserved since the homeowner merely lived in the property, sometimes making zero improvements and degrading every appliance with time and usage. Home equity is generally determined by the aggregate of comparable market sales. But homes are far from apples-to-apples comparisons. There are major upkeep or replacement costs that come with roofs, HVACs, foundations, and plumbing/electrical. Yet, home values are now almost solely determined by the location and square footage.

What should be a depreciating asset is now an equity printing machine that could translate to free real estate with enough time and currency degradation. Homes literally pay for themselves if the equity matches the total cost of the mortgage and any upkeep.

The average median price for a home in America has doubled in less than 10 years. Some homeowners may find their equity triple the original purchase price of the home before they’ve paid off a third of the loan. In the right market someone could utilize their home equity to buy multiple properties in cash while never paying off the original mortgage.

The older generations like to justify this privilege by stating that the cost of lending used to be much higher, so the cost of living then was analogous to today’s. While it is true that mortgage rates were higher, the rate of appreciation outpaced any interest expense, so the principle could be paid off long before the end of the loan’s term. They never actually paid that interest. They likely rolled their equity into numerous other residences, and maybe a couple vacation homes, while constantly refinancing to take advantage of the same cheap interest rates that ballooned the value of homes they never actually owned.

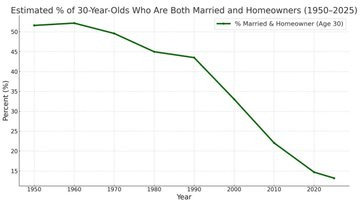

Homeownership is the primary tool to build wealth, so when this privilege is harder to reach for each generation, we find a major wealth gap emanating between those who own and those who could never hope to own. This gap is further widened by Wall Street landlords who abuse this system to purchase hundreds or even thousands of homes to charge absurd rent to families and service their overleveraged real estate portfolios that banks give them the privilege of pretending to own.

How do you fix this Ponzi scheme cultivated by loans created from nothing to aggrandize the value of assets that people need to survive?

It is clear that we need to be part of this scheme or else be crushed by it, so we will demand our government give us the same privilege afforded to the prior generations. That means more subsidized loans at abysmally cheap rates to ensure that everyone is entitled to the same Ponzi. The aforementioned solution is just more gasoline on the real estate forest fire, so they will need to come up with more clever schemes to keep up the charade.

An asset bubble inflated with cheap debt and easy access to equity will require exponential amounts of both to ensure the perpetuity of undeserved wealth attained by securing mortgages typed into existence.

They will begin by offering zero down payment mortgages with 50-year terms. They could even subsidize the first few years of interest at the expense of the taxpayer, just like student loans. The burden of government debt will be astronomical, so they will have to start issuing U.S. Treasury bills attached to more speculative assets to keep interest rates low.

This is not hypothetical. It is already rumored that the federal government will begin issuing bonds with Bitcoin and other cryptocurrencies attached. They carry the option to capitalize on any upside appreciation of the underlying asset while absorbing all the downside risk. The yield on the bond itself will be 1% or less to manipulate the “risk-free rate” on long-term bonds. Mortgage rates on other consumer debt will follow to keep lending cheap and dependent on the future earnings of every taxpayer.

Simultaneously Wall Street will begin tokenizing real estate on blockchain ledgers so that home equity is easily accessible, transferable, and dividable into fractional ownership. You’ll be able to buy and sell fractions of a percent of any real estate property on a moment’s notice. Your own home equity will be transferable currency. Homeownership will be determined by the majority shareholder.

This is the corner we backed ourselves into by treating homes like an investment instead of a place to live and raise a family.

The real way to save the housing market is to get the banks and the government out of the equation.

We must build new and independent communities that do not rely on state/municipal infrastructure or business centers. These would be self-sustaining unincorporated townships with mixed residential and commercial use. They would have to generate their own power, collect their own water, and utilize the existing land and mineral resources that come with the property.

The value of homes would be determined by the cash flow generated by the estate rather than the underlying asset. The free market would determine the price of homes, but financing would be done strictly in-house and lent by other homeowners in the community. This means people would get to source their own neighbors and be beholden to those people for the right to live on and work the land. Lending requirements would be determined by the community instead of a soulless entity.

This is how we bring humanity back into homeownership. They tried to convince us that we need these intermediaries called banks to facilitate the building and financing of homes. They were always using our deposits to fund the mortgages of our neighbors, but once they got the legal right to counterfeit money, asset values lost all semblance of reality.

Thus, the risk of default was too great, and we required the government to absorb that risk with our collective taxes. Now homes can only be acquired by subscribing to an elaborate Ponzi scheme that steals the value of our work to ensure that criminal counterfeiting organizations are paid for homes they never deserved to own.

The value of the home was always determined by what you could do with it. The worth of the land was based on what the people residing on it were able to bring to the broader community.

Our concept of real estate has been contorted by paper value denoted in a dying currency. We think we are getting rich, but this wealth is undeserved and will curse us for generations.

I found a lot to like about this article, however, the author would do well to more clearly distinguish between individuals and groups.

"While it is true that mortgage rates were higher, the rate of appreciation outpaced any interest expense, so the principle could be paid off long before the end of the loan’s term. They never actually paid that interest. They likely rolled their equity into numerous other residences, and maybe a couple vacation homes, while constantly refinancing to take advantage of the same cheap interest rates that ballooned the value of homes they never actually owned."

Unless you sell the home, you absolutely have paid that interest.

I bought my house 36 years ago and will likely never sell it. Price appreciation has done (and likely will do) nothing for me, except increase my taxes and insurance.

My original loan was at 10.5% -- and those mortgage payments came out of my paycheck and from no one else. High interest was a great motivator to pay off that loan early.

There is very little one can say about a group (homeowners) that is meaningful to an individual (homeowner).